Germany's Auto Suppliers Rank 2nd in Sales. Last in Profits

17 of the world's biggest suppliers are German. So why is their typical margin just 1.7%?

Ad

This issue is supported by Berylls by AlixPartners

For this issue, I spoke to Jürgen Simon. He co-authored the new TOP-100 supplier study from Berylls by AlixPartners. His analysis and the study’s data run throughout.

Berylls by AlixPartners had no editorial influence over this issue.

Welcome to Issue #121 of The German Autopreneur.

In 2025, the world built more cars than the year before. And yet the combined revenue of the world’s 100 largest suppliers fell. More cars, less money.

Germany is hit the hardest. 17 German companies rank in the top 100. That puts Germany 2nd by revenue. And yet German suppliers have the thinnest margins of any major supplier nation.

They still sell a lot. More than almost anyone. They just don’t make money anymore. And if they don’t rebuild their businesses now, they won’t be around much longer.

I looked at the new TOP-100 supplier study from Berylls by AlixPartners and spoke to Jürgen Simon. He’s one of its authors.

In this issue:

Why suppliers now earn more than the manufacturers they supply, for the first time in years

Why German suppliers are down to 1.7% margins

What Japan and China do differently. And how Germany can find its way out

Suppliers Now Earn More Than Manufacturers

That sounds backwards. For the first time in years, the average supplier earns more than the manufacturer it supplies:

Suppliers: 5.2% margin (down from 5.8%)

Manufacturers: 4.2% (down from 6.9%)

2 very different stories drive those numbers.

1) Manufacturers are having an especially hard time. There’s intense global price competition. Add geopolitical tensions and tariffs. And on top of that, they still have to invest billions in future technologies.

2) Not all suppliers are the same. “Supplier” is just a catchall (from chipmakers to seat manufacturers). A few are doing very well and pulling the average up. Others barely earn anything.

What separates winners from losers? Not who sells the most. 3 things matter most:

What you build

Where you build it

Who you sell to

And on all 3 counts, German suppliers are in a weak position:

Many build what’s earning the least right now

They often produce where it’s expensive

Their most important customers are German automakers, and those are struggling the most

The result: the typical German supplier (median) is left with 1.7% margin.

The Segment Decides Everything

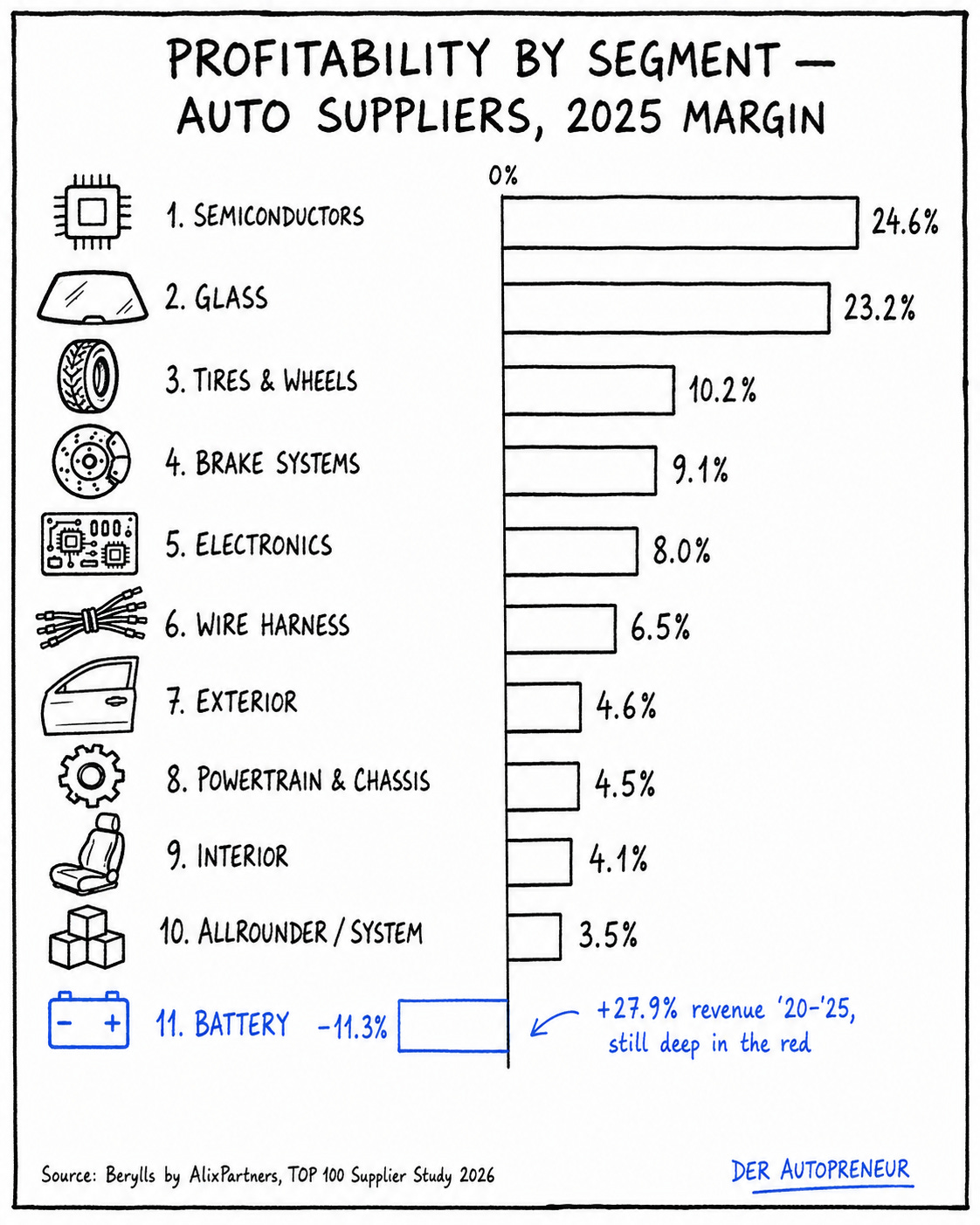

Just how big is the gap? Look at the typical margin by segment:

Strong: semiconductors 24.6%, glass 23.2%, tires 10.2%

Weak: powertrain 4.5%, batteries -11.3%

Some segments make serious money. One is actually burning cash. And of all things, it’s batteries. The segment everyone considers the future.

The interesting detail: no segment has grown faster in revenue than batteries. They’re up +27.9% per year since 2020. And no segment has worse margins.

How is that possible when more EVs sell every year?

Building batteries means putting billions into massive factories upfront. Those factories aren’t running at full capacity. EV demand grew more slowly in 2025 than planned.

On top of that, falling cell prices are squeezing margins. Companies sell more and still make almost nothing. Jürgen summed it up: sectors like batteries and electronics sold very well. But that doesn’t automatically mean profit.

South Korea shows what that looks like. They’re stuck at 2.9% margin because the major battery manufacturers are deep in the red.

China is different. Market leaders like CATL don’t publish margins, but are seen as clearly profitable.

The lesson: the wrong segment drags down an entire nation’s average.

German Suppliers Barely Make Money Anymore

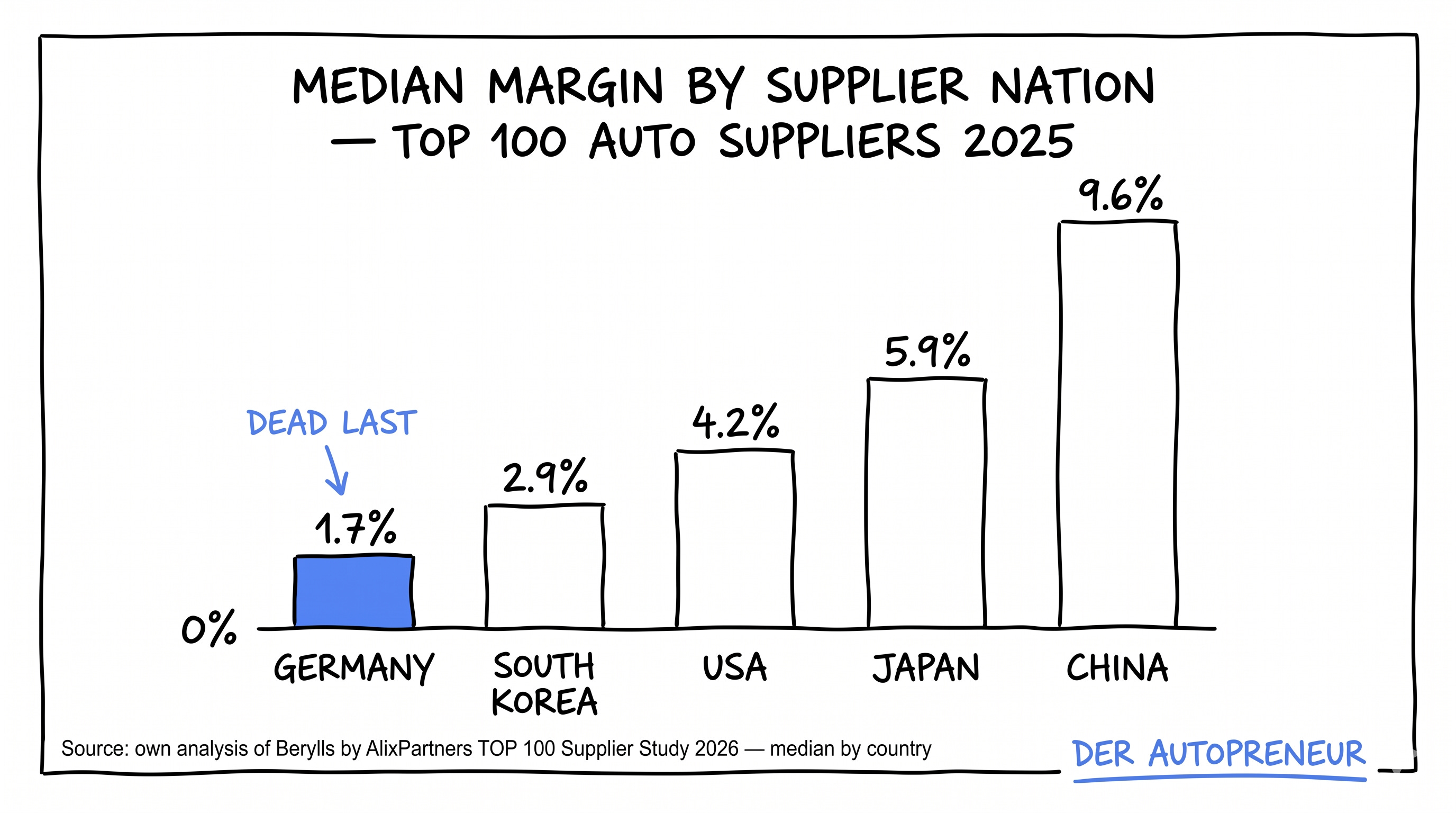

It shows up most clearly in Germany:

2nd in revenue

Last in margins

That’s the worst result of any major supplier nation.

You can see it with Bosch. Around $60 billion in revenue. By far the world’s largest auto supplier. And the margin: 1.8%.

The main reason is the segment. Germany’s biggest suppliers are heavily tied to traditional powertrain. That’s everything around the combustion engine. And that segment is weakening. 5 of the 10 lowest-margin companies in the top 100 are German.

2 German companies side by side show why the segment matters so much:

ZF in traditional powertrain: -2.8% margin

Infineon in semiconductors: 21.5%

Location is the other factor. Producer prices in Germany rise around 6.7% per year. In China: 0.8%.

What that looks like in practice: in 2025, 10 factories closed in Germany and just 1 opened. Germany is the only major region where more plants are closing than opening.

The thin margins are becoming a real problem for many. To get through it, these companies need to rebuild their businesses. That costs a fortune. It can’t come from the business itself. They don’t earn enough. The only option: take on debt.

But when you barely make money and are already heavily indebted, banks aren’t offering much:

Either no credit at all

Or only at very high interest rates

At exactly the moment they need money most, it’s at its most expensive.

Berylls by AlixPartners expects a wave of bankruptcies and mergers through 2027/28.

Japan Earns 3x What Germany Does

The comparison with Japan is striking. Japan is actually very similar to Germany: an old, strong combustion-engine nation with well-established manufacturers and suppliers. Japan has 21 suppliers in the top 100. Germany has 17.

And yet the typical Japanese supplier earns 5.9% margin. More than 3 times what a German supplier earns.

How is that possible, with such similar starting conditions?

It’s not about the product. It’s about the relationship between manufacturer and supplier.

In Japan, manufacturers and suppliers work together. The relationships are close and built on mutual respect. Companies often hold stakes in each other.

The manufacturer doesn’t just squeeze prices. Both sides get through the rough years together.

In Germany, it’s the opposite: take it or leave it. If you supply Mercedes, VW, or BMW, you’re just a cost to cut. Pressure gets passed straight down the chain. I hear this from suppliers constantly.

And that’s dangerous. We in Germany are destroying our own supplier base piece by piece. Germany needs these suppliers for development and production. And we’re the ones pushing them out of the market.

Same starting conditions. Completely different relationship with the customer. That 3x gap is entirely self-inflicted.

China Earns the Most and Grows the Fastest

And China? You’d expect brutal price competition, nobody making money. It’s the opposite:

15 companies in the top 100, 3 of them new this year

+11.0% revenue growth for the typical company

9.6% margin (median), roughly 5 times what Germany earns

One caveat: only 7 of the 15 Chinese companies actually report their margins. Major players like CATL aren’t included here.

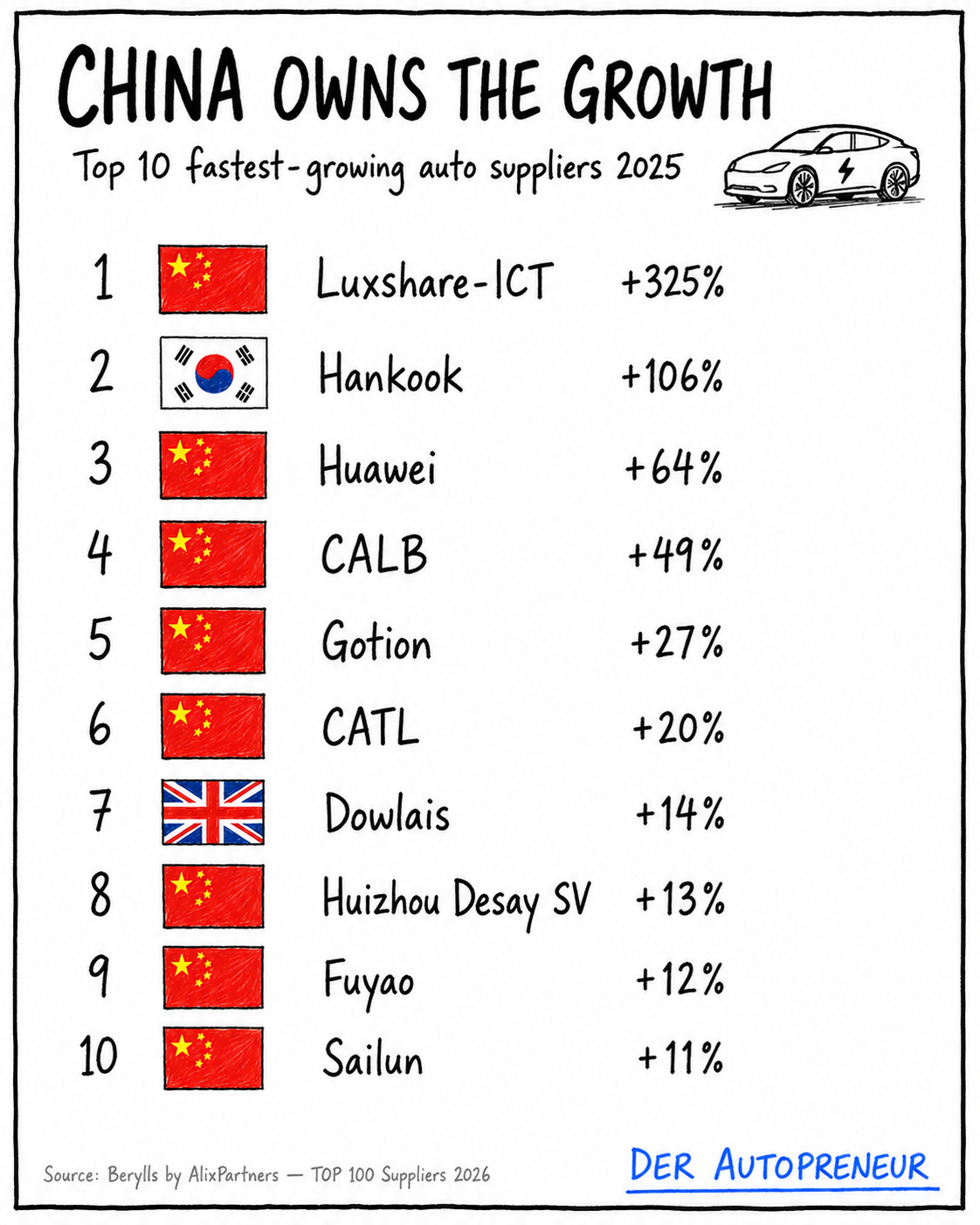

But the speed is what’s really unsettling. China is growing fastest:

8 of the 10 fastest-growing suppliers in the world are Chinese

By revenue, China has just overtaken the US and now sits at 3rd place, right behind Germany and Japan

Until now, China’s growth has come mainly at Japan’s expense. Since 2020, Japan has lost 6 spots in the top 100. China has gained 8. Germany has held its 17.

The question is how long that lasts. Jürgen’s assessment: holding on to those 17 spots will be “very difficult.”

How German Suppliers Can Still Survive

For German suppliers, it’s no longer just the margin under pressure. It’s the business model itself. From 3 directions at once:

Their core business is shrinking. Everything around the combustion engine is in decline

Chinese suppliers are taking market share. Even German manufacturers are increasingly buying from China

Chinese automakers are becoming more important as customers. But they’re more vertically integrated and buy less from outside. And when they do, they prefer Chinese suppliers

Getting cheaper or better isn’t enough anymore. Jürgen’s words: “The old German premium supplier model has to change, at least in part.”

So there are 2 directions:

Expand into more profitable segments

Or exit automotive entirely and move into new markets

What the restructuring looks like in practice:

ZF is selling its entire driver assistance division to Harman for around $1.6 billion. That cuts its debt

Continental is spinning off its entire automotive business as Aumovio

Mahle is building cooling modules for stationary battery storage systems

Schaeffler is making components for humanoid robots and cooling technology for data centers

The AI boom is both a threat and an opportunity. Data centers are buying up the chips the automotive industry needs. But that same wave creates an opening: suppliers who build components for those data centers benefit disproportionately.

My Take

For me, this won’t be decided by the numbers. It’ll be decided in people’s heads.

German suppliers had a stable business for decades. Same customers, same market. Our industry is cyclical: you move from one crisis to the next. But until now, each was temporary. You got through it by becoming more efficient and cheaper. Then things picked back up. The business model itself was never in question.

This crisis is different. Getting more efficient isn’t enough this time. For the first time in generations, these companies have to rethink what they actually do.

And they can. Bosch, Continental, ZF. Some have been around for over 100 years. They all started with a bet: someone took a risk and saw a market that didn’t exist yet. The quiet decades came after. The job changed: optimize, manage.

That’s exactly where they need to go back. From manager to founder. The hard part isn’t figuring out which segment is performing. The hard part is this shift in mindset. Getting curious again. Being brave again. Making bets again. And most of all: learning how to learn again. What do I bet on? What do I let go of? Where do I want to be in 10 years?

Jürgen put it bluntly: “The core isn’t necessarily what I’ve been doing for the last 100 years.” This is “far from a temporary dip.” It’s “more like a new reality.”

Realistically, that means: in a few years, maybe fewer than 17 German companies will still sit in the top 100. That doesn’t have to be bad news. Some might be missing simply because they found a far more profitable business outside automotive. And the ones that remain will be making money again. Not because they were the biggest. But because they made the right bet at the right time.

🔗 Berylls by AlixPartners TOP 100 Supplier Study 2026

A note on methodology: Margins by nation reflect the typical company (median), not the average. Individual figures may therefore differ from the study’s published numbers.

That’s all for today.

Until next week,

Philipp

PS: If you find value here, share it with someone who should read it too.

Want to work with me?

I help global B2B companies connect with 100,000+ automotive decision makers in Germany.

Nice! I'm reading now the book Numbers don't lie, by Vaclav Smil, and among many things, he defends that still manufacturing things is what makes a country rich. Software doesn't employ so much people, and manufacturing distributes profits better.

Philipp, thank you once again for presenting us with a very interesting article, particularly for me, who works within the ecosystem of a German automotive group and has been closely following this entire global situation. My interpretation remains the same: the European problem is not a lack of sales, customers, or even technical skills. The problem is that the European economic model has stopped working. Europe absolutely needs to reinvent itself if it wants to try to stay alive in this fight. Another point in the article that caught my attention was the following: "Chinese market leaders like CATL don’t publish margins, but are seen as clearly profitable." It is necessary to pay attention to the fact that Chinese numbers are not always as transparent as European or American ones. And here comes a point that many Western analysts mention: the Chinese state can distort reality. However, what convinces me most that the Chinese threat is real is not actually the margins of its companies. It's another piece of data from your article: eight of the ten fastest-growing automotive suppliers are Chinese. Even if the exact margins are debatable, the growth in industrial capacity, exports, investment in technology, and market share gains are a very visible phenomena and difficult to disguise for years. That said, and as much as I distrust the exact margins presented for some Chinese companies, I distrust even more those who think that Chinese industrial growth is just propaganda. The challenge for Europe is real, and we have to know how to adapt and reinvent ourselves. Thank you again, Philipp.