Oops, I Did It Again. Europe Just Lost the Self-Driving Race

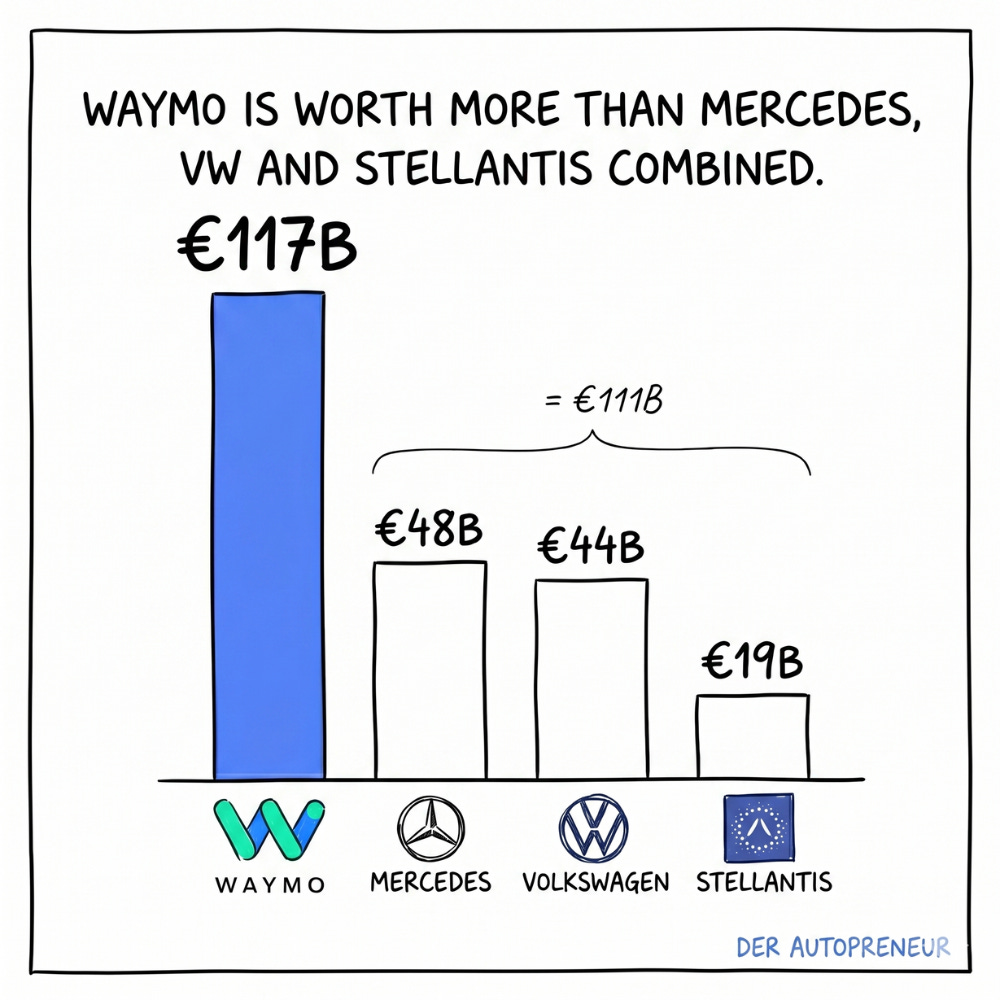

$21B poured into self-driving in 4 months. Waymo is now worth more than Mercedes, VW, and Stellantis combined.

Sponsored

UDS was never built for software-defined vehicles

Vehicle diagnostics was designed for the combustion era. UDS is the standard used today to read and flash ECUs. But modern vehicles run on central compute, get over-the-air updates, and communicate via software interfaces. A different world.

The new standard is SOVD: Service-Oriented Vehicle Diagnostics. Built for software-defined vehicles. An official ISO standard since March. The first OEMs are already rolling it out.

If you own diagnostics or SDV at an OEM or Tier-1: On June 2 at 14:00 CEST, there’s a free webinar.

DSA Group Aachen has worked on vehicle diagnostics for decades and will show what works, where it breaks, and how SOVD can sit alongside your UDS setup.

Welcome to Issue #119 of The German Autopreneur.

15 years ago, German carmakers faced a decision. Build it themselves? Or buy it? The answer: buy. It’s just a commodity.

Today the battery is the most expensive part of an EV. And most of it comes from China. The industry feels those consequences every day.

That same pattern is repeating right now. This time with self-driving.

Your own car. The taxi you hail. The bus you take to work. All 3 will drive themselves in the coming years. And the technology behind it probably won’t come from Europe.

Today I’ll show you:

How a research curiosity became a real market overnight

Why this market is actually 3 different markets

And how Europe is sliding into the next big tech dependency

Self-Driving Is Here Now

For years the line was: self-driving will come eventually. In early 2026, it arrived.

In the first 4 months, $21B poured into the market. More than 2024 and 2025 combined. Waymo alone raised $16B and is now worth $126B. More than Mercedes, VW, and Stellantis combined.

And this time, the money is no longer chasing hype. In 2024, 127 companies raised fresh capital for self-driving. In 2026, only 34. But total funding didn’t shrink. It’s 4 times larger. 3 of every 4 dollars go to Waymo. The winners are emerging.

The technology is being built in 2 places. The US and China. But it doesn’t stay there.

In the US, Waymo runs about 500,000 paid rides per week. Across 10 US cities. London and Tokyo come online this year.

In China, Apollo Go, Pony(.ai), and WeRide are on the road. Apollo Go in Wuhan. Pony(.ai) in Beijing, Shanghai, Shenzhen, and Guangzhou. WeRide in more than 40 cities worldwide.

Why is it suddenly moving so fast? Cost. Apollo Go builds its robotaxi for $28,000 today. Sensors and chips included. A robotaxi already costs less than most new private cars.

The experimental phase is over. But in Europe, not a single robotaxi operates without a safety driver.

3 Markets for Self-Driving. Europe Only Plays in 1

Use these 3 markets to make sense of every self-driving story in the years ahead.

Market 1: The private car

This is about private cars that drive themselves. The market closest to the traditional auto industry. 2 strategies are in play.

Strategy 1: Build everything in-house. Their own chips, their own software, their own car. Tesla, Xpeng, NIO, and Li Auto take this path. All of them are based in the US or China.

Strategy 2: Buy it. Every European automaker takes this path. I’ll show you how in a moment.

Market 2: The robotaxi

This is about cars you order through an app. No driver. They take you from A to B. Usually within a city.

US: Waymo, Tesla, Zoox

China: Pony(.ai), WeRide, Apollo Go

In London, 4 robotaxi services launch side by side this year:

Waymo with its own app

Uber with software from Wayve

Apollo Go through Uber and Lyft

Pony(.ai) via Bolt

And in the EU? The first commercial robotaxi service runs in Zagreb, Croatia. Operator: Verne. The vehicles: Arcfox from BAIC. The virtual driver: Pony(.ai). Both from China. Stellantis is building the same setup in Luxembourg. Also with Pony(.ai).

Market 3: The shuttle

This is about self-driving minibuses. They run fixed public transit routes at low speeds.

This is where Europe is supposedly ahead:

MOIA from VW operates in Hamburg, Germany

KIRA from Deutsche Bahn operates in Langen, near Frankfurt

HOLON from Benteler launches in Jacksonville, Florida, in late 2026

But all of them run with a safety driver. And none of them builds its own virtual driver. They buy it from Mobileye in Israel. On top of that, they build the rest of the service themselves: vehicle, route, app, operations.

Even Mobileye itself doesn’t yet operate anywhere without a safety driver.

The only German startup with its own technology is MOTOR Ai in Berlin. They call themselves Germany’s Only Full-Stack Level 4 AV Startup.

Money Is Moving From Cars to Software

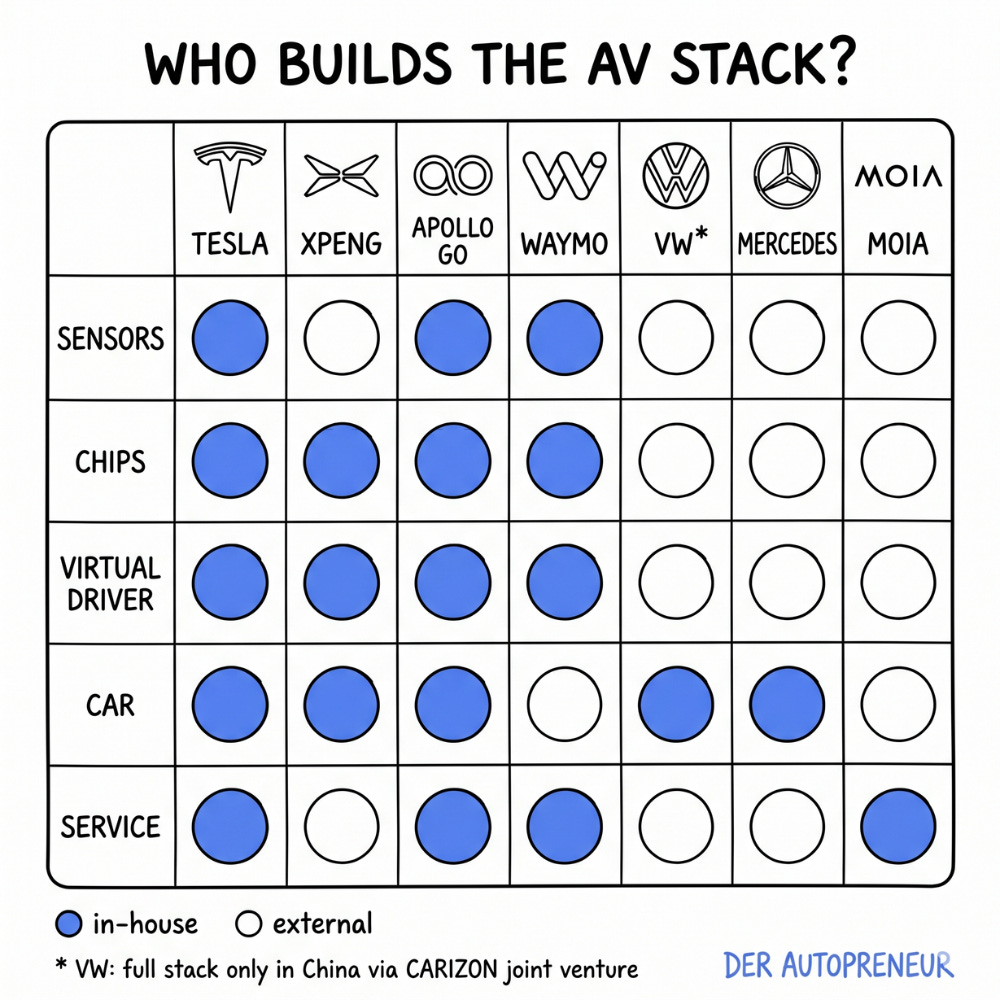

To play in any of these markets, you need 5 building blocks in the car:

The sensors. Cameras, LiDAR, radar. The eyes and ears of the car.

The compute chips. They process all sensor data in real time.

The virtual driver. The software and AI that actually drives the car.

The car itself.

The service. App, fleet, pricing, cleaning, support. Everything around the ride that touches the customer.

On top of that, 3 more things:

Cloud compute to train the AI

Experts who develop the AI

A lot of capital. 10 to 15 years before the first dollar comes back

This is exactly where the battery pattern repeats. In a combustion car, the engine was the core and the most expensive part. In an EV, that role moved to the battery. In a self-driving car, it moves to the virtual driver.

And the virtual driver probably won’t be built 3 times. Once for the private car, once for the robotaxi, once for the shuttle. Once one player builds it cheaply at scale, that player serves all 3 markets.

It’s like Google licensing Android to dozens of phone makers. Tesla already runs the same software in private cars and robotaxis. In China, Xpeng licenses its virtual driver to VW. Whoever has the best and cheapest virtual driver wins in all 3 markets.

Anyone who doesn’t build the virtual driver themselves depends on a supplier for the most valuable part of the car.

On top of that, robotaxis will take over part of urban mobility. And whoever uses one orders it through an app. That app usually doesn’t belong to the automaker. It belongs to Uber, Lyft, or Bolt.

So value is moving away from automakers in 2 directions:

Upstream to the technology players who sell them the virtual driver

Downstream to the platforms that own the customer relationship

What’s left in the middle: building the car.

Where Do German Automakers Really Stand?

The bottom line up front: Mercedes, BMW, and VW still develop in-house up to Level 2. At Level 4, they don’t.

Why not? Because it’s very expensive and very slow. Waymo has existed since 2009. Alphabet has invested billions over 15 years. Only now are they starting to commercialize. No publicly traded European company waits that long for revenue. And Europe doesn’t have venture capital on a US or China scale.

In Q1 2026, Waymo raised $16B. Wayve raised $1.5B. Germany’s hope, MOTOR Ai, raised $18M.

With that gap, only one conclusion follows. German automakers can’t build the Level 4 virtual driver themselves. So they buy it.

Mercedes and BMW:

Both shut down their own Level 3 programs in early 2026. The reason: Level 3 became irrelevant. The industry is moving directly from Level 2 to Level 4

Both still have in-house solutions up to Level 2. Anything beyond that, they buy

Mercedes uses NVIDIA globally. Momenta in China. Plus a stake in Wayve in London

BMW uses Qualcomm and Mobileye. Also Momenta in China

Volkswagen:

In Europe and the US: CARIAD develops software for Level 2 and 3. Qualcomm supplies the high-performance chips. Audi, Bentley, and Porsche also use Mobileye. The MOIA shuttles run on Mobileye too

In China: VW paid $1B for a stake in Horizon Robotics. In their joint venture CARIZON (60% VW, 40% Horizon), the 2 companies develop software up to Level 2 and their own chips. VW also buys solutions from Xpeng and ZYT

Bosch:

Bosch and CARIAD have developed software for VW group brands together for years. Based in Germany. Up to Level 3. Level 4 is explicitly off the table

For robotaxis, Bosch supplies sensors, brakes, and compute. Bosch does not build the virtual driver

The picture is the same everywhere. For the most valuable building block, every German automaker depends on a supplier. From the US, Israel, China, or the UK. From the EU: nobody.

So Who Is Building the European Solution?

3 companies are trying.

Wayve in London:

In February 2026, Wayve raised $1.5B. Valuation after: $8.6B. Investors: Mercedes, Stellantis, Nissan, Uber, NVIDIA, Microsoft, SoftBank

Europe’s biggest hope. With 1 catch: they’re based in the UK, outside the EU

MOTOR Ai in Berlin:

The only German startup trying to build the full stack itself. Sensors, chips, virtual driver. Their own technology for Level 4

On funding, they’re in a different league from Waymo or Wayve. But the only team in Germany with this ambition

Verne in Zagreb:

In April 2026, Verne launched the first commercial robotaxi service in the EU. Robotaxis powered by Pony(.ai). From China. Still with a safety driver for now

Background: Verne received about $190M in EU funding. The condition: the technology had to be European. The original plan was for its own robotaxi with Mobileye as the virtual driver

But the in-house development wasn’t ready in time. 5 days before the funding deadline, Verne announced the partnership with Pony(.ai) and Uber. 1 day before the deadline, the first paid ride took place. With a robotaxi from China

I wrote about this on LinkedIn a few weeks ago. In the comments, the CEO clarified that the EU funding went exclusively to in-house development. The Chinese robotaxis were paid for with private capital from external investors. According to him, the 2 buckets stayed strictly separate.

Whether that explanation holds or not, Verne represents a pattern. Europe can’t get its own technology on the road in time. And in the end, the order goes to China.

My Take

15 years ago, with the battery, German carmakers could still say they didn’t see it coming. With self-driving, Europe shouldn’t make the same mistake. The shift is happening in real time. Europe could push back. But it isn’t.

How? China and the US show how.

China keeps foreign technology out. Not through a single law, but through several rules:

Data can’t leave the country

Only licensed companies can create maps

Every software update needs prior approval

That’s why Mercedes, BMW, and Audi have to buy their China software from Momenta. They don’t have a choice.

The US blocks Chinese robotaxi technology outright. Chinese software is banned from 2027. Chinese hardware from 2030. The main argument: national security.

The other clear driver: protecting their own industry. Robotaxis will be a cost game. Whoever scales cheapest wins. And at scale, nobody will match China.

Open your market to China now, and no domestic industry will emerge. The US understands that.

Europe could do the same. One rule would be enough. Anyone who wants to run a self-driving service in Europe has to use European technology. Private car, robotaxi, or shuttle.

That would be a political decision. It would trigger private investment in a European industry overnight.

It won’t be made.

With the battery, we couldn’t fully see the consequences 15 years ago. This time, we can. And we’re watching it happen anyway.

PS: Big thanks to Daniel Abreu Marques for the conversation that shaped this analysis.

🔗 re | way | dam2 | ele1 | rt | hr | tnw | dam | bis

That’s all for today.

Until next week,

Philipp

PS: If you find value here, share it with someone who should read it too.

Want to work with me?

I help global B2B companies connect with 80,000+ automotive decision makers in Germany.

What if self driving never works or makes a vehicle too expensive?